“Even though I keep a household budget, I can’t really see the effect…”

“I want to manage my household finances more efficiently and reduce unnecessary spending!”

Many people share these concerns. Managing household finances is an ongoing challenge for many. It’s easy to put it off or give up after just a few days… But wait! By properly understanding and categorizing the basics of household budgeting—fixed costs and variable costs—you could dramatically improve your financial situation.

I’ve heard of fixed and variable costs, but what’s the exact difference? How should I categorize them to make household budgeting more effective?

This article will answer those questions. From the basic definitions of fixed and variable costs to practical categorization methods and household budgeting tools, I’ll explain everything in a clear and easy-to-understand way. By reading this article, you will:

- Clearly understand the difference between fixed and variable costs

- Learn how to categorize them to suit your household

- Discover specific ways to identify and reduce unnecessary expenses

- Manage your household finances more efficiently using budgeting tools

This article is packed with valuable insights to enhance your budgeting skills. So, start today—master fixed and variable costs, and take control of your finances smartly and enjoyably!

Language: English Japanese

1. What Are Fixed and Variable Costs?

As a first step in household budget management, you often hear, “Let’s separate fixed and variable costs!” It’s generally explained as “distinguishing between expenses based on whether the amount paid each month is fixed or variable.”

For example, take “utility costs.” The amount changes every month, yet many household budgets classify them as fixed costs. “Huh? They fluctuate, but they’re fixed costs?” I was also confused at first.

So, I did some research and organized the definitions of fixed and variable costs into two approaches. In Chapter 1, I will explain these two definitions in an easy-to-understand manner using concrete examples. You should be able to clearly understand and say, “Oh, that’s what it was all about!”

1-1. Definition of Fixed Costs

“How much money do I regularly spend each month?” Have you ever wondered that? When managing a household budget, the first thing to understand is “fixed costs.” I categorized the definition of fixed costs into two approaches.

Definition 1: Fixed Amount

In this definition, fixed costs refer to expenses that remain the same each month. Examples include the following costs. These expenses are typically withdrawn from your account or paid every month in nearly the same amount.

- Housing costs (Rent, mortgage payments, condo fees, parking fees)

- Insurance premiums (Life insurance, health insurance, car insurance, etc.)

- Communication costs (Fixed plans, home internet service)

- Tuition fees for lessons

- Subscription service fees (Fixed rate)

The advantage of understanding fixed costs with this definition is that it makes predicting monthly expenses easier. By knowing the minimum required amount, planning a household budget becomes more straightforward. For example: “Since fixed costs are 150,000 yen per month, we can allocate the remaining income to variable costs and savings.”

However, there are some points to keep in mind with this definition. For example, if you switch your smartphone plan from a flat rate to a pay-as-you-go plan, communication costs become variable costs. Additionally, if you move and your rent changes, the amount of fixed costs will also change. In other words, fixed costs are not permanently set—they need to be reviewed periodically.

Definition 2: Essential for Living

In this definition, fixed costs refer to expenses that are essential for living and occur regularly each month. Examples include the following costs.

- Housing costs(Rent, mortgage payments, condo fees, parking fees)

- Utilities (Gas, electricity, water)

- Communication costs (Smartphone plan, home internet service)

- Insurance premiums (Life insurance, health insurance, car insurance, etc.)

Unlike Definition 1, this definition also classifies utilities and communication costs as fixed costs. This is because they are essential for daily life and occur every month. Even if the amounts fluctuate, these expenses are difficult to reduce, so they are considered fixed costs.

The advantage of using this definition is that it clarifies the minimum expenses required to maintain a living. This helps you identify the threshold that absolutely cannot be reduced and manage your household budget more realistically.

1-2. Definition of Variable Costs

When you feel like “I might have overspent this month…” it’s time to review your variable costs. I categorized the definition of variable costs into two approaches.

Definition 1: Costs that vary in amount

In this definition, variable costs are expenses that fluctuate in amount each month. Examples include the following costs. These expenses can vary significantly depending on your actions and circumstances each month.

- Food expenses (Groceries, dining out, coffee shops)

- Utility costs (Gas, electricity, water)

- Transportation costs (Gasoline, train/bus fares based on usage)

- Entertainment expenses (Books, movies, travel, classes)

- Social expenses (Weddings, funerals, gifts)

- Daily necessities (Toiletries, cleaning supplies, etc.)

- Clothing expenses (Cloth, shoes)

- Medical expenses (Doctor visits, prescriptions)

The advantage of using this definition for variable costs is that it helps you easily identify areas where you can save. It allows you to take concrete actions, such as “I ate out a lot this month, so I’ll cook more at home next month” or “I bought too many clothes this month, so I’ll cut back next month.”

Definition 2: Costs that can be managed in daily life

In this definition, variable costs are expenses that can be adjusted through your own efforts and choices. Examples include the following costs.

- Food expenses (Groceries, dining out, coffee shops)

- Transportation costs (Gasoline, train/bus fares based on usage)

- Entertainment expenses (Books, movies, travel, classes)

- Social expenses (Weddings, funerals, gifts)

- Daily necessities (Toiletries, cleaning supplies, etc.)

- Clothing expenses (Cloth, shoes)

- Medical expenses (Doctor visits, prescriptions)

- Subscription service fees

Unlike Definition 1, subscription service fees are considered variable costs because they can be canceled or adjusted by changing plans.

The advantage of using this definition for variable costs is that it reinforces the mindset of “I can reduce expenses through my own efforts.” This can boost your motivation to cut wasteful spending and save more by reducing unnecessary expenses.

1-3. Summary of Definitions

To summarize the key points of the definitions, they are as follows:

Definition 1: Categorizing Based on Whether the Amount Is “Fixed” or “Variable”

Fixed costs: Expenses that remain the same amount every month.

Variable costs: Expenses where the amount fluctuates from month to month.

With this definition, the key factor is whether the expense amount remains constant or changes over time.

| Fixed | Variable |

|---|---|

|

Housing costs Communication costs (fixed plans) Insurance premiums Tuition fees for lessons Subscription service fees (fixed rate) |

Food expenses Utility costs Transportation costs Entertainment expenses Social expenses Daily necessities Clothing expenses Medical expenses |

Definition 2: Categorizing Based on Whether It Is “Essential” or “Manageable”

Fixed costs: Expenses that are essential for living and occur regularly.

Variable costs: Expenses that can be adjusted based on personal efforts or choices.

With this definition, the key factors are “whether the expense is essential” and “whether you have control over it.”

| Fixed | Variable |

|---|---|

|

Housing costs Utility costs Communication costs Insurance premiums |

Food expenses Transportation costs Entertainment expenses Social expenses Daily necessities Clothing expenses Medical expenses Tuition fees for lessons Subscription service fees |

Note that the classification of the same expense item may change depending on which definition you use. For example, utility costs are considered variable costs in Definition 1 and fixed costs in Definition 2. It’s not a matter of which definition is better or worse; instead, choose the one that best suits your household budget management style.

2. The Benefits of Separating Costs

This chapter explains the specific benefits of separating fixed and variable costs in your household budget. It focuses on the following four key advantages:

- Easier expense tracking

- Long-term savings through fixed cost reduction

- Prevention of wasteful spending by managing variable costs

- Simplified budget setting

Understanding these benefits will enhance your motivation for household budget management and provide concrete methods for achieving more effective savings.

2-1. Easier Expense Review

What exactly am I spending my money on, and how much?

Even if you keep a household budget, your overall expenses might seem vague, making it hard to know where to start making changes. Have you ever felt that way? Separating fixed and variable costs provides a clearer picture of your spending, making it much easier to identify areas for improvement.

By recording fixed and variable costs separately, you can see at a glance how much money is going out each month as fixed costs and how much fluctuates from month to month as variable costs. This makes it easier to develop specific strategies, such as “My fixed costs are this amount, so I need to reduce my variable costs,” or “Among my variable costs, food costs are particularly high, so I’ll try to eat out less.”

Furthermore, managing fixed and variable costs separately makes it easier to compare them with past spending. You’ll be more likely to notice changes, such as, “Compared to last month, my fixed costs haven’t changed, but my variable costs have increased,” or, “I reduced my fixed costs, which led to a decrease in my overall spending.” This approach allows you to identify areas for improvement in your household budget management more effectively.

In this way, separating fixed and variable costs is an effective method for accurately understanding your household finances and identifying potential issues more easily.

2-2. Fixed Cost Reduction Leads to Long-Term Savings

Isn’t there a way to reliably save money, even just a little, every month?

When you hear the word “saving,” you might imagine cutting back on food expenses or giving up things you want—sacrifices that require constant effort in your daily life. However, by reviewing your fixed costs, you can achieve long-term, reliable savings with a one-time effort.

For example, if you review your smartphone plan and switch to a plan that is 2,000 yen cheaper per month, you will save 24,000 yen per year and 120,000 yen over five years. This significant savings from a one-time effort is a unique advantage of reducing fixed costs.

Additionally, fixed costs are more likely to be reduced significantly at once compared to variable costs. For example, you could substantially lower your monthly expenses by reviewing your housing costs, moving to a property with lower rent, or refinancing your mortgage.

Of course, reviewing fixed costs takes time and effort. However, it’s well worth it. Reducing fixed costs is a powerful saving method that can have a significant positive impact on your household finances in the long run.

2-3. Control Variable Costs to Prevent Wasteful Spending

I tend to spend money wastefully… How can I learn to manage my money more systematically?

Everyone has likely experienced buying unnecessary items at a convenience store or making impulse purchases in daily life. By becoming aware of and controlling your variable costs, you can reduce wasteful spending and learn to manage your money more systematically.

To manage your variable costs, it’s essential to first understand where your money is going and how much you’re spending. By recording and regularly reviewing the breakdown of your variable costs, you can gain insights such as, “I ate out frequently this month” or “I spent too much on clothing.” Based on these insights, it’s important to set and implement specific goals, such as “I’ll limit eating out to once a week next month” or “I’ll avoid buying new clothes this month.”

It’s also effective to set a budget to control your variable costs. By establishing a budget in advance, such as “Keep food expenses within 30,000 yen this month” or “Limit entertainment expenses to 10,000 yen,” you can prevent overspending. Controlling variable costs requires daily awareness and effort, but it is a crucial step in reducing wasteful spending and improving your household finances.

2-4. Easier Budget Setting

I want to manage the balance between my monthly income and expenses more effectively… How can I save money reliably and without undue stress?

The goal of household budget management is to control expenses within your income and save money. To achieve this, it’s important to first set a realistic and achievable budget. Separating fixed and variable costs makes budgeting much easier.

Since fixed costs are expenses that occur regularly, you need to know their amount when setting a budget. Once you know your fixed costs, the “minimum amount you need each month” becomes clear. Next, you set a budget for variable costs. Since variable costs change from month to month, you should set an amount that you feel you can reasonably achieve by referring to past spending data.

Then, the amount remaining after subtracting the budgets for fixed and variable costs from your income is the amount you can save. This becomes your realistic savings goal. If you need to further reduce your expenses to achieve your savings goal, consider reviewing your fixed costs or cutting back on your variable costs.

In this way, by separating fixed and variable costs, you can easily understand the balance between your income and expenses and set a budget that allows you to save money reliably and without undue stress. Additionally, setting a budget will increase your motivation for household budget management and allow you to work more actively toward achieving your goals.

3. Utilizing Household Budgeting Tools

Once you understand how to separate fixed and variable costs, the next step is to put that knowledge into practice. You might be wondering, “What kind of tool should I use?” In this chapter, I’ll introduce the original “KAKEIBO” series of budgeting tools, which I developed based on many years of budgeting experience and expertise with Excel.

With these tools, anyone can easily apply the concepts of fixed and variable costs to their daily budget management. The lineup includes “KAKEIBO PRO” and “KAKEIBO LiGHT,” which are ideal for detailed analysis, as well as “KAKEIBO SLiM,” which stands out for its simplicity. Learn about the features of each and discover the tool that’s best suited to your needs.

3-1. Utilizing KAKEIBO PRO/LiGHT

I want to keep a budget, but I’m worried it will get messy with too many items… Isn’t there a way to manage my spending in more detail, but still keep it organized?

If you want both detailed analysis and ease of organization, KAKEIBO PRO and KAKEIBO LiGHT are perfect for you. Their biggest strength is that they let you manage expenses in two stages: “categories” and “expense items”.

First, you classify your spending into broad categories such as “Housing” or “Food”, and then designate each one as either a fixed cost or a variable cost. This helps you grasp the overall flow of your money from a high-level perspective—for example, “My variable costs were high this month.”

Next, within each category, you create more specific expense items such as “Groceries”, “Dining Out”, or “Cafes”. This makes it easier to identify the root of spending issues—for instance, “My food costs are high because I spent too much on dining out!” From there, you can develop targeted improvement plans.

In short, KAKEIBO PRO and LiGHT allow you to see the big picture while also conducting detailed analysis—that’s their true strength.

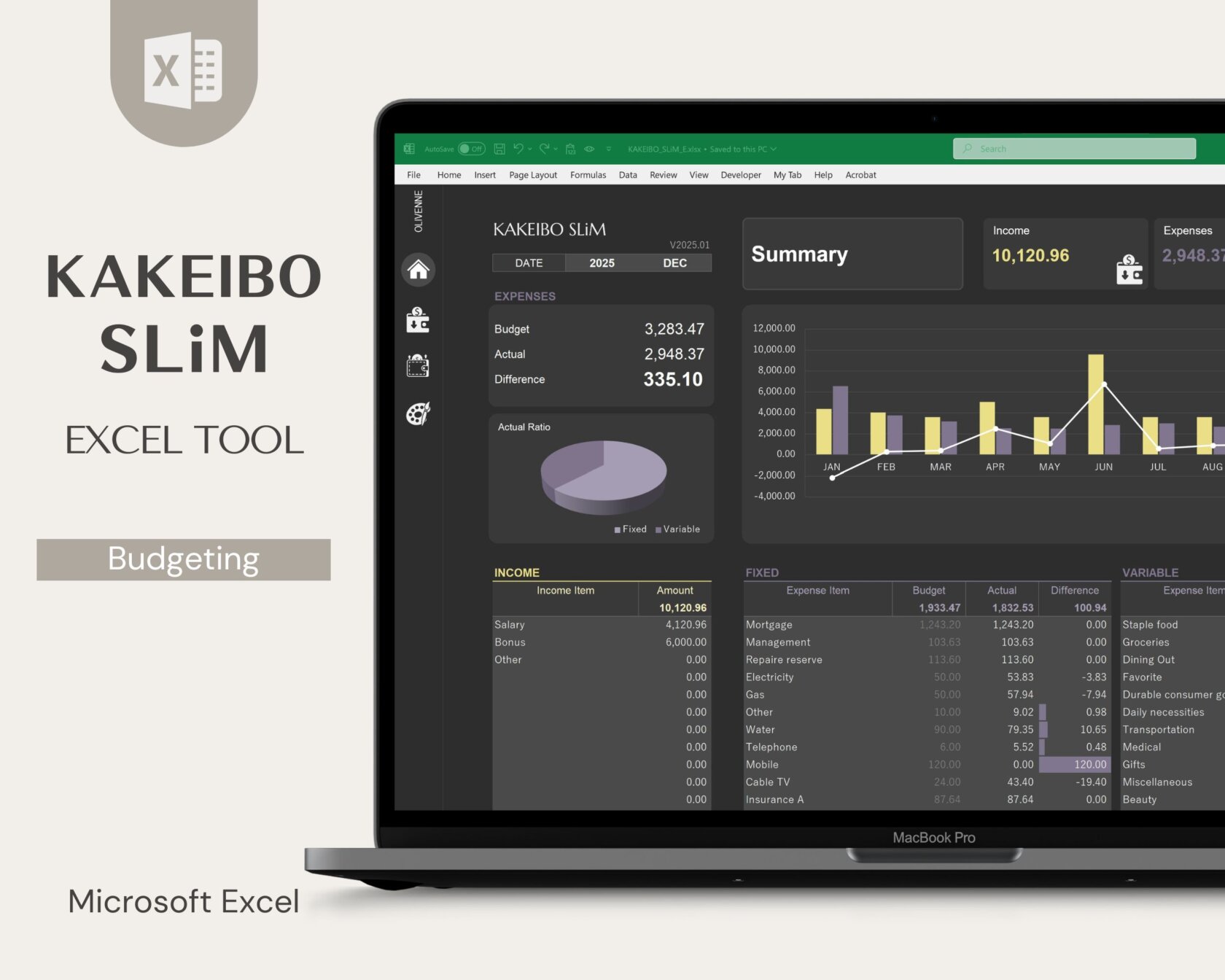

3-2. Utilizing KAKEIBO SLiM

Having many features is nice, but the initial setup seems like a hassle… I just want a simple way to get into the habit of tracking my spending!

For you, I recommend KAKEIBO SLiM, a tool designed with ultimate simplicity in mind. Unlike PRO or LiGHT, KAKEIBO SLiM doesn’t require a category setup. Instead, it has a straightforward structure where you directly set up specific expense items—such as Rent, Food, and Transportation—within the two main classifications of Fixed Costs and Variable Costs.

Thanks to this simplicity, the initial setup is quick, and daily entries are easy. Its greatest advantage is that it’s easy to stick with—even for people who usually give up on budgeting after just a few days. It’s the perfect tool for beginners who are thinking, “First, I just want to build the habit of tracking my expenses,” or “It’s enough if I can get a general idea of my cash flow.”

Although the features are simple, KAKEIBO SLiM still achieves the most important goal of budgeting: understanding your spending. Start by building the habit of using KAKEIBO SLiM, and you’ll soon gain valuable insights into your spending patterns.

4. Conclusion

Before reading this article, the concept of fixed and variable costs may have seemed a little difficult or tedious. But now that you understand the differences between them—and why separating them is so important—I hope you’re thinking, “I can do this!”

Household budgeting is more than just recording expenses. By visualizing your spending through the separation of fixed and variable costs, it becomes surprisingly easy to see where waste is hiding and where you can start saving effectively. Fixed costs can lead to long-term savings with just a single review, while variable costs can be managed through small, daily adjustments. Simply becoming aware of these two categories can transform your cash flow.

Now that you have the knowledge, it’s time to put it into practice. Why not start by taking the first step in a way that feels easy for you, using the budgeting tools introduced here as a guide? There’s no need to aim for perfection from the beginning. Just focus on the simple mindset of separating your expenses. That will be the most important and reliable first step toward achieving your ideal household finances.

I sincerely hope that managing your budget becomes both more effective and more enjoyable—starting today.

Related Articles